Using Life Insurance to Generate Tax-Free Income in Retirement

Most people take out a life insurance policy to protect the people they love in case something happens to them. But certain types of life insurance...

We all know long-term care (LTC) policies can provide tax-free benefits on the money “out,” but are you aware of the tax advantages available when paying money “in?”

Financial advisors who understand and leverage LTC tax differentials can open valuable planning conversations with individual clients, business owners, and professional networks.

At Core Income, we go beyond simply quoting products – we help advisors connect LTC tax benefits with meaningful client strategies. In this article, we’ll explore how you can help your clients take advantage of tax-deductible opportunities with LTC, grow their funds tax-free, and maintain tax-free benefits on the backend.

Table of Contents

Why is This Important for Financial Advisors?

Over the past decade, the insurance industry has seen a significant shift, with many insurers moving away from traditional LTC policies and focusing on hybrid products. This shift means your clients now need more guidance on navigating the tax deductibility of premiums under various IRS guidelines.

We’ve found that many people are not aware of opportunities to deduct premium payments for hybrid LTC products, potentially missing valuable tax benefits. Advisors can help their clients take steps early to improve the tax efficiency of funding the policy—maximizing deductions on the front end while ensuring that back-end benefits remain tax-free.

Connecting with your professional network of CPAs and estate planning attorneys also opens new opportunities to discuss tax-saving strategies that appeal to their clients.

Business owners are ideal candidates for these discussions—not only because of their business income but also their higher individual income and assets. By demonstrating ways to maximize business-related tax benefits, you offer value that other advisors might overlook. This is a unique opportunity to position yourself as a specialist in tax-advantaged strategies that benefit both the business and the individual.

Introducing these strategies to CPAs and attorneys makes it easy for them to recognize when to bring you into conversations, opening the door to valuable discussions with new clients and prospects. At Core Income, we’ve worked with companies to implement policies for top executives, often converting those business relationships into individual planning clients.

When CPAs or attorneys work with clients looking to reduce their tax burden, they’re more likely to refer them to you as a resource for LTC tax strategies. These conversations can help you generate new clients and strengthen your role as a tax-aware advisor within your professional network.

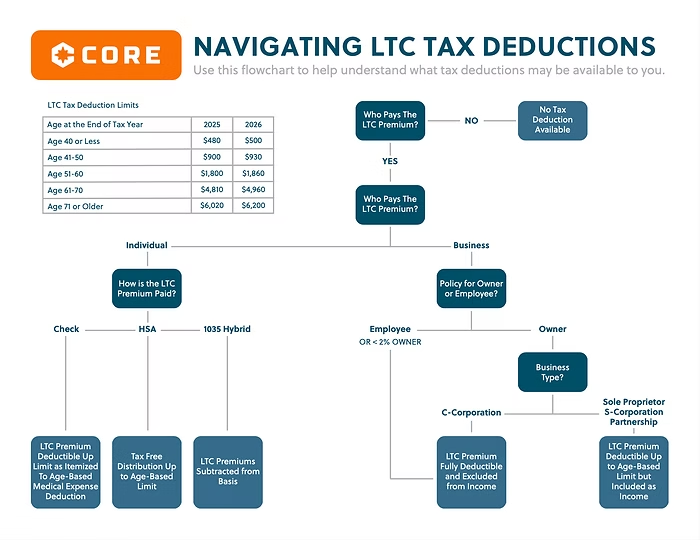

Download our Flowchart: Navigating LTC Tax Deductions

Our flowchart, Navigating LTC Tax Deductions, is one of our most popular resources for advisors. Consider it a quick-reference tax guide tailored to LTC and linked-benefit conversations. This one-page flowchart provides an easy-to-follow decision tree to help you determine deductibility based on specific client scenarios.

Whether you keep it on your desk or share it with your professional network, this guide is designed to make complex tax information accessible and highlight how these benefits can provide substantial leverage for your clients. Plus, we can white-label the chart with your logo for a personalized touch—just email marketing@coreincome.com if you’d like it customized for your brand.

What is a Hybrid Long-Term Care Policy?

Hybrid LTC insurance combines the benefits of LTC insurance with permanent life insurance or an annuity. These policies allow clients to pay a designated premium as a lump sum or in installments in exchange for support with future LTC needs.

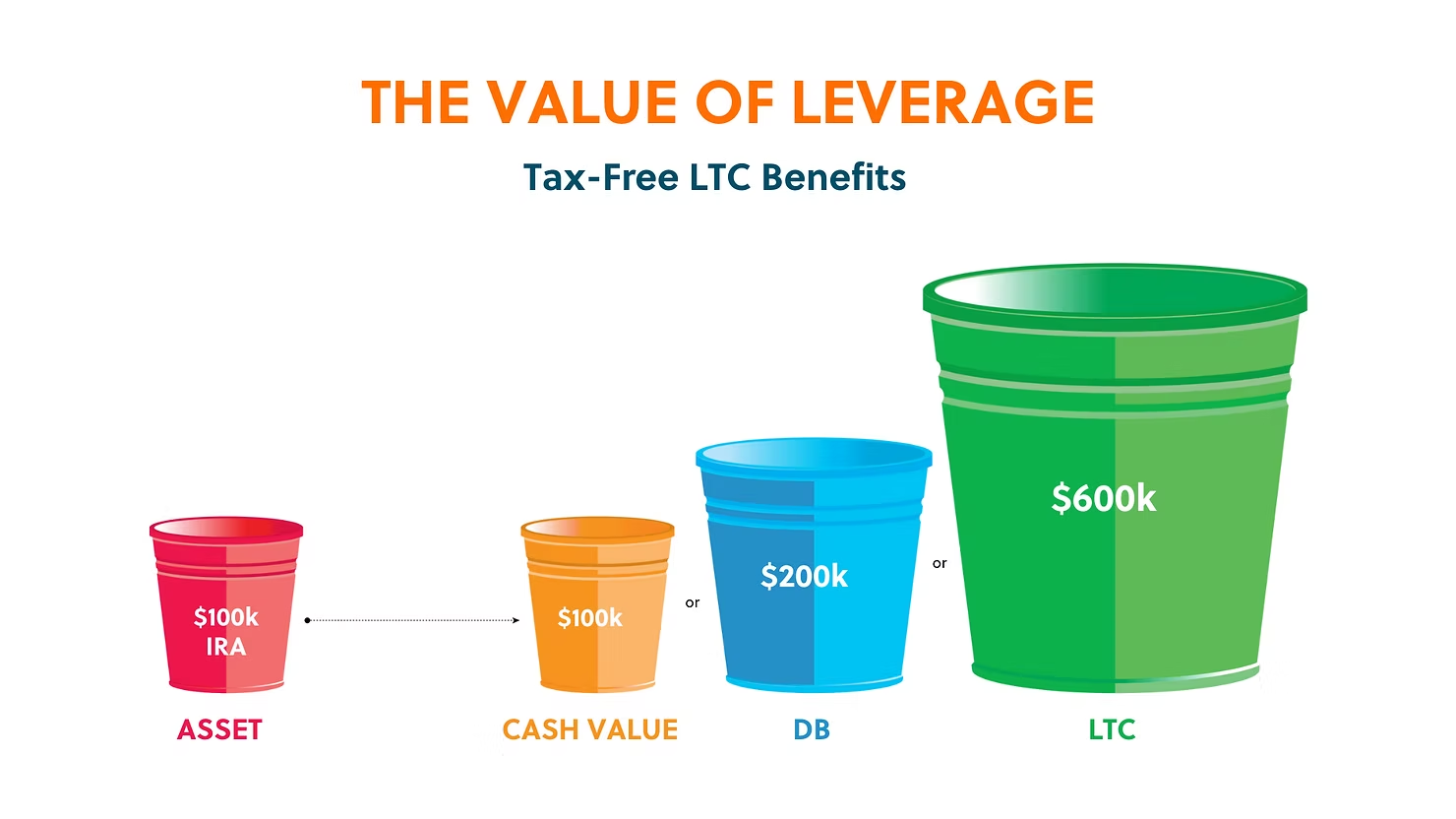

Clients generally have two options when paying for long-term care: insure against these costs with leverage or self-insure by drawing from their assets dollar for dollar. Hybrid LTC policies offer a unique solution by allowing clients to reposition an existing asset, transforming it into a leveraged resource for LTC that can provide significantly more coverage on the back end and be tax-free.

For example, consider a married, 60-year-old couple in reasonable health with $100,000 in assets. By shifting this amount into a hybrid LTC policy, they can enhance their LTC protection while preserving other assets (as illustrated in the graphic above). Here’s how a hybrid LTC policy can work for them:

Long-Term Care Tax Deductions for Individuals

Individuals who purchase LTC insurance policies for themselves, their spouses, and their tax dependents may deduct the premiums as personal medical expenses, provided they itemize their tax returns.

However, these deductions are only applicable if the individual’s total unreimbursed medical expenses exceed 7.5% of their adjusted gross income (AGI).

Additionally, the amount of premium that can be deducted is subject to specific dollar limits based on the insured's age at the end of the tax year.

Hybrid or traditional LTC policies offer potential tax deductions for individuals, though eligibility depends on a few key factors. Here are the three main steps to determine the income tax deduction for premiums:

Determine the Amount of LTC Premium Paid: For hybrid policies, you must be able to distinguish between the premium portion allocated to the base life insurance policy and the premium for the LTC extension policy. Only the LTC portion qualifies for potential tax deductions. If the insurer doesn't separate these premiums, you won't be able to claim the deduction.

Review Limitations: The IRS sets age-based limits on how much of an LTC premium can be deducted, which generally increase with age and adjust for inflation each year. The policy must also meet IRS requirements for "qualified" LTC insurance, including providing specific care services, guaranteed renewability, trigger requirements, and more. Write it off as a Schedule A medical expense by itemizing, meaning the client must be upwards of $13,000/year in write-offs as an individual or $26,000/year for couples.

Write it off as a Schedule A medical expense by itemizing, meaning the client must be upwards of $13,000/year in write-offs as an individual or $26,000/year for couples.

Exceed the 7.5% AGI threshold for medical expenses.

Apply the Medical Expense Deduction Limit: For individuals who itemize deductions, LTC premiums can be included in unreimbursed medical expenses. These premiums are tax-deductible when total unreimbursed medical expenses exceed 7.5% of their AGI. However, the deductible amount for LTC premiums is capped at the lesser of the premium paid or the IRS age-based limit.

Examples:

Mike, Age 55:

Mariana, Age 72:

When structuring a policy for tax efficiency, clients who want to maximize tax benefits might allocate more of the premium to the LTC component and reduce the life insurance base. If the tax deduction isn't as important, it would be better to front-load the life insurance policy, with less going into long-term care.

Using a Check to Fund Long-Term Care Premiums (Individuals)

For individual clients, achieving LTC tax benefits by writing a check is very limited. Most retirees who write a lump-sum check for an LTC policy are focused on the leverage and tax deductions on the back end rather than the tax benefits on the front end.

For example, consider a 65-year-old client writing a lump sum non-qualified check for $100k. This could purchase a six-year LTC pool worth $464k, and all $464k can be returned to them tax-free. Here’s how it’s broken down:

While the LTC premium portion is technically deductible up to the IRS age-based maximum, this deduction is often out of reach. If the 65-year-old client put $43k into an LTC policy, they could write off $4,710 of the LTC premium. However, to claim this, the client must:

In practice, even if a client meets these criteria, a one-time deduction of $4,710 would yield only about $1,015 in tax savings, making it a modest benefit for most clients.

This limited tax benefit is why we don’t often emphasize this scenario.

Using a Health Savings Account to Fund Long-Term Care Premiums (Individuals)

For individuals, using Health Savings Account (HSA) funds to cover LTC premiums can be a valuable tax strategy. This can be an important conversation for advisors, especially with clients in their 40s or 50s who aren’t ready to buy an LTC policy yet but could benefit from building up their HSA. Here’s why:

Using a 1035 Exchange to Fund Long-Term Care Premiums (Individuals)

A 1035 exchange allows individuals to transfer existing life insurance or annuity policies into hybrid LTC policies. When you move from life to hybrid, it’s not a tax deduction, but rather, it’s a tax-free exchange since you’re getting additional leverage.

A hybrid LTC policy can be structured as a life insurance policy with an LTC rider or an annuity with an LTC extension, both of which allow benefits to be accessed tax-free.

For example, suppose a client purchased a non-qualified annuity in 1980 for $50,000, and due to market growth, it’s now valued at $150,000. With this gain, the client faces a substantial tax liability if they withdraw the funds or pass them on to their heirs, who would inherit the tax burden. However, by transferring (or "1035 exchanging") this annuity into a qualified annuity LTC policy, the client can leverage the full $150,000 for long-term care benefits, and all gains can be used tax-free for LTC expenses.

In the right LTC policy, the $150,000 initial investment could even be leveraged up to $450,000 in LTC benefits, all accessible tax-free. This is an excellent strategy for clients with appreciated annuities they may not need for income.

With annuities, ownership can often be adjusted before the 1035 exchange. A single-owned annuity can be changed to joint ownership with a spouse, allowing both to be covered under the hybrid LTC policy.

Life insurance can also be transferred via a 1035 exchange into a life-LTC hybrid. However, only the insured can remain covered in the transfer of single or whole-life policies. Joint coverage isn’t possible unless both spouses are already on the original policy (second-to-die).

Business-Sponsored Long-Term Care Policies

Offering LTC policies through a business can create unique opportunities for tax savings and employee retention, such as:

Let’s take a closer look at each of these scenarios.

Long-Term Care Tax Deductions for C-Corporations

The C-Corp structure offers the most potential for businesses to maximize LTC deductions.

When a C-Corp purchases LTC insurance for its employees (including owner-employees), their spouses, or dependents, the company can deduct 100% of the premiums as a business expense, with no limitations.

These employer-paid premiums are not included in the employee’s taxable income. However, any life insurance component in the policy will remain taxable for the policy owner.

C-Corps, typically larger corporations, have utilized executive bonus plans to secure greater tax deductions for the business while reducing taxable income for key employees. These plans provide tax efficiency and income exclusions, making them a valuable tool for employee retention.

Long-Term Care Tax Deductions for Pass-Through Entities

Most small businesses are typically some type of pass-through entity, which includes:

In pass-through entities, the business gets to write off the entire premium – life insurance and LTC. For the employee, life insurance is included in taxable income, but LTC is not.

For an owner-employee, life insurance is included in taxable income up to the age-based limit, but LTC is not. As such, the owner or employee could pay for the life portion with personal funds, and it would not be taxable income at that time.

Sole Proprietors and 2% (or Greater) Owners of S-Corps and LLCs

The tax code determines tax liabilities within S-Corps and LLCs by examining the individual's ownership in the company. Employees who own 2% or more of the S-Corp or LLC are deemed owner-employees.

Since owner-employees of S-Corps and LLCs are considered self-employed for tax purposes, they follow the same tax deductibility for LTC insurance as sole proprietors:

When a company covers LTC premiums for a sole proprietor or owner-employee (and potentially their spouse and dependents), these premiums are deductible by the business as long as the company retains no interest in the policy.

However, the full amount of the LTC premium paid by the company is added to the owner-employee's gross income, as well as any premiums paid for their spouse or dependents, but is deducted as a health expense up to the age-based max.

2% (or Smaller) Owners of S-Corps and LLCs

The tax code classifies individuals who own less than 2% of an S-Corp or LLC as regular employees. In this scenario:

When a company purchases an LTC policy for its employees, the entire premium amount, including both the life insurance and LTC components, is deductible by the company.

This would also apply to the premiums paid on behalf of an employee's spouse and other dependents. Only the life insurance portion is considered taxable income for the employee.

Partnerships

Companies structured as partnerships can deduct LTC premiums as an ordinary business expense when purchasing a policy for a business partner, spouse, or dependent. Employer-paid LTC insurance premiums are not included in the employee's gross income.

For the business partner receiving the LTC benefit, the entire premium paid by the company is includable in their gross income as a guaranteed payment. This holds true for partnership-paid premiums paid on behalf of the partner’s spouse or dependents.

In this case, the partner is treated as a self-employed individual for tax purposes, and the LTC premiums received would be subject to the same tax rules as those applied to pass-through entities in the prior section.

How Core Income Can Help

We're here to help ensure your product designs meet your clients' needs and maximize their tax deductions.

As a financial advisor, you can start by reaching out to younger clients to discuss taxes and financial planning while educating business owners on the benefits of LTC policies. Connecting with business owners, especially those with excess earnings, can expand your reach to high-net-worth individuals.

If you're interested in hosting seminars on LTC tax deductions for your clients or professional network, we can help you master these concepts.

Remember to share our flowchart with your professional network. Collaborating with CPAs and estate planning professionals can position you as a valuable resource for their business-owner clients.

To learn more about how we can help you maximize your clients’ tax benefits, schedule a meeting with one of Core Income's founders, Tim Foley, or call us at 800.541.7713.

--

Core Income is an FMO, IMO, and independent insurance brokerage dedicated to serving financial advisors, their staff, and their clients.

Our mission is to help advisors deliver financial certainty by supporting them through actuarial precision, elite responsiveness, and collaborative partnerships.

To learn more about how we can support you, schedule a consultation with our team or call us at 800.541.7713.

Stay connected with us on social media for more tips and insights on annuities, life insurance, and long-term care.

Insurance policy guarantees are subject to the financial strength and claims-paying ability of the issuing insurance company. The death proceeds will be reduced by a long-term care or terminal illness benefit payment under this policy. Clients should consult a tax advisor regarding long-term care benefit payments, terminal illness benefit payments, or when taking a loan or withdrawal from a life insurance contract. Please keep in mind that the primary reason to purchase a life insurance product is the death benefit. Life insurance products contain fees, such as mortality and expense charges, and may contain restrictions, such as surrender periods.

This material may contain a general analysis of federal tax issues. It is not intended for, nor can it be used by any taxpayer for the purpose of avoiding federal tax penalties. This information is provided to support the promotion or marketing of ideas that may benefit a taxpayer. Taxpayers should seek the advice of their own tax and legal advisors regarding any tax and legal issues applicable to their specific circumstances. These materials are for informational and educational purposes only and are not designed, or intended, to be applicable to any person’s individual circumstances. It should not be considered investment advice, nor does it constitute a recommendation that anyone engage in (or refrain from) a particular course of action.

Most people take out a life insurance policy to protect the people they love in case something happens to them. But certain types of life insurance...

For certain clients, particularly those with little risk of outliving their assets, claiming benefits earlier can result in higher lifetime wealth,...

The holiday season is an excellent opportunity to express appreciation for your clients. However, we recognize it can quickly become overwhelming...