Top Retiree Regrets: How Advisors Can Protect Clients with Mathematical Certainty

According to a comprehensive study by the Transamerica Center for Retirement Studies, a leading research organization in retirement planning, only...

Updated: February 27, 2026

Inflation is often referenced as the silent killer of financial planning—and for good reason.

While compound interest is regarded as one of the best things for clients during their accumulation years, it can become one of their most significant challenges in retirement. Just like interest, inflation compounds over time, but during the multiple decades of your clients’ retirement years, it works in the opposite direction. It works against your clients by steadily eroding their purchasing power during what should be their golden years.

Despite this, inflation remains one of the most underweighted factors in retirement planning, leaving many retirees vulnerable to spending shortfalls. Without proper planning, financial advisors may face difficult conversations with clients, like explaining why they’ll need to cut their spending back by $20,000 a year because inflation estimates fell short.

Preparing for higher inflation rates is crucial to safeguarding your clients’ financial security. In this article, we’ll explore how inflation impacts your clients’ finances over their lifetimes and how you can help manage this risk. By doing so, you can ensure that your clients’ retirement plans are built to withstand inflationary risks and protect their spending power.

Table of Contents

How Does Inflation Work Against Your Clients in Retirement?

Although inflation may seem like a basic concept most people are familiar with, its long-term impact on retirement plans is often underestimated. To truly understand its effects, we must explore what happens when clients transition from building wealth to spending it.

For most clients, retirement is the ultimate destination. During their working years, the accumulation phase, they focus on saving and investing, leveraging the power of compound interest to grow their wealth.

By investing early, clients allow their money to grow exponentially as they earn interest on their principal, then interest on the interest, and so on. Over decades, this compounding effect significantly accelerates wealth creation.

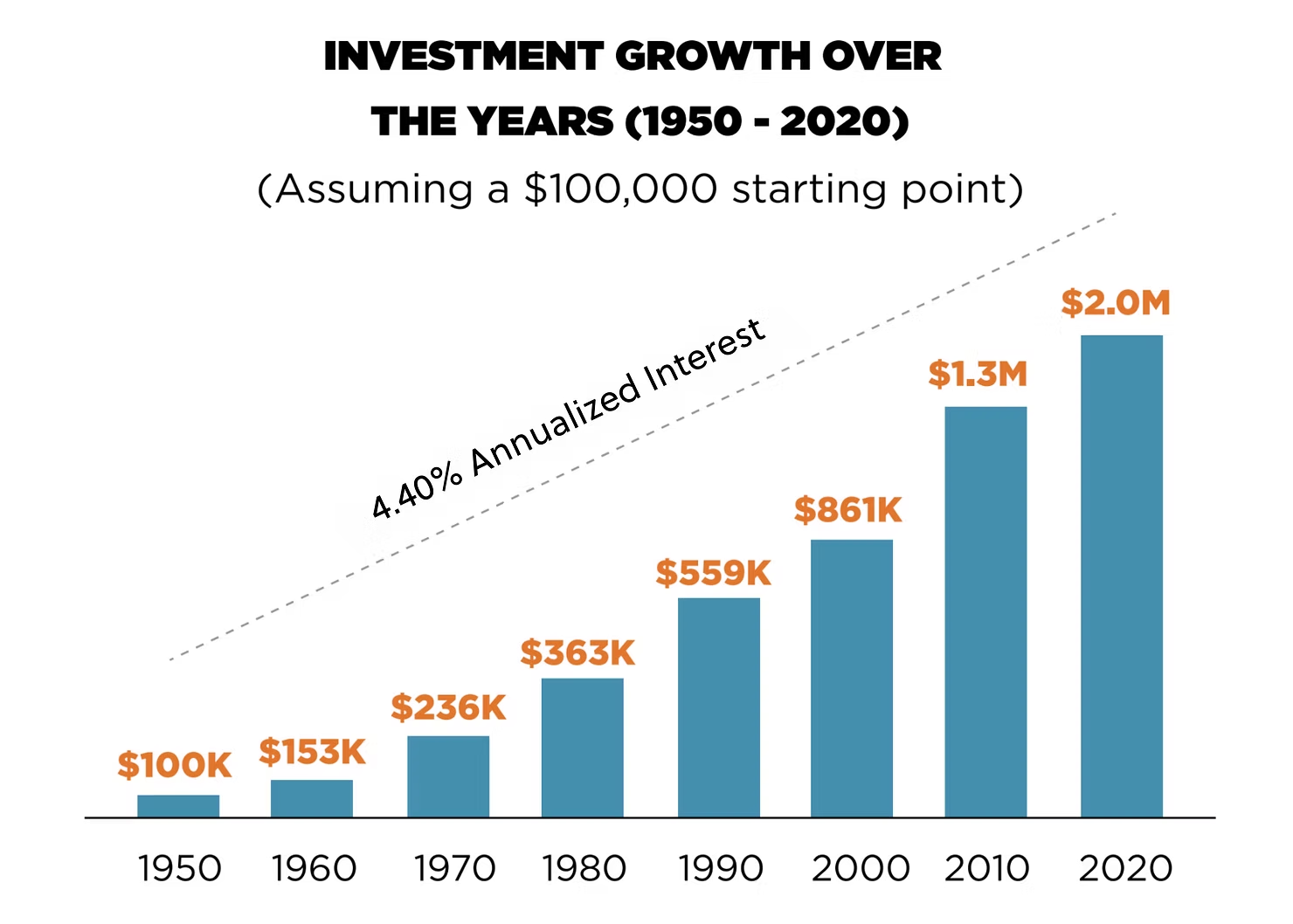

For example, if you had a client who invested $100,000 in 1950 with an annualized inflation rate of 4.4%, that money would have grown to $153,000 after a decade, earning $53,000 of interest in that one decade. Your client is earning interest on the interest in the compounding effect. As wealth continues to build, their interest credits in the seventh decade (2010 to 2020) totaled $700,000 in that one decade. This is 14 times the amount of interest earned in that first decade.

The Flip Side of Compound Interest in Retirement

Once your clients retire, their financial focus shifts. They want to relax and take it easy—it’s what they’ve worked hard to achieve! However, this is also when compound interest starts to work against them. Here’s why:

How Inflationary Risks Affect Client Portfolios: A Comparison Between 2% and 3% Inflation Assumptions

To safeguard your clients’ retirement income, it’s crucial to design portfolios that balance growth, income, and inflation protection. Traditionally, this has been achieved using a 60/40 portfolio split— 60% equities and 40% bonds. Two primary purposes drove the idea of moving from equities to bonds:

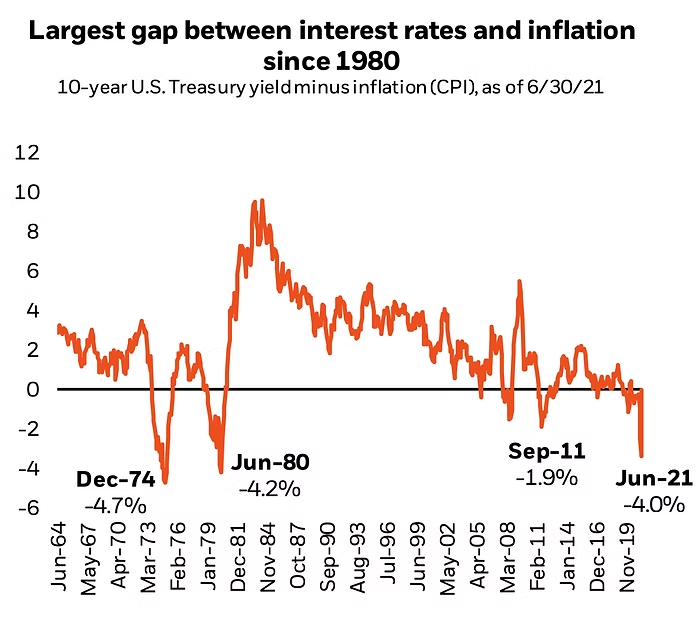

However, economic shifts in the past few years have complicated this traditional approach. Historically, inflation and fixed-income yields have moved in tandem. For instance, during periods of low inflation, interest rates were also low. Yet, in 2021, inflation surged to 4–6% annually, while fixed-income yields remained low, creating a significant gap not seen since the 1970s. This disconnect poses challenges for advisors aiming to protect clients from inflation’s erosive impact.

How can advisors build and adjust portfolios that protect their clients? While long-term equities can offset inflation, allocating all of a client’s assets to equities is also not feasible

from a market risk standpoint. So, what does an actuarial-constructed retirement portfolio look like?

Here’s how a typical client’s retirement portfolio might look in practice:

retirement portfolio might look in practice:

A 66-Year-Old Couple with a $1,000,000 Portfolio:

Explore inflation scenarios for your clients using our Inflation Tool through Actuary Lab. To learn more about this tool, check out this article which offers sample reports, a video walkthrough, and a detailed explanation of how it can deliver financial certainty in retirement planning for you and your clients.

If you’re using financial planning software like Advisor Controls, e-Money, MoneyGuidePro, RetireUp, Retirement Analyzer, etc., we can help you incorporate these concepts into your software.

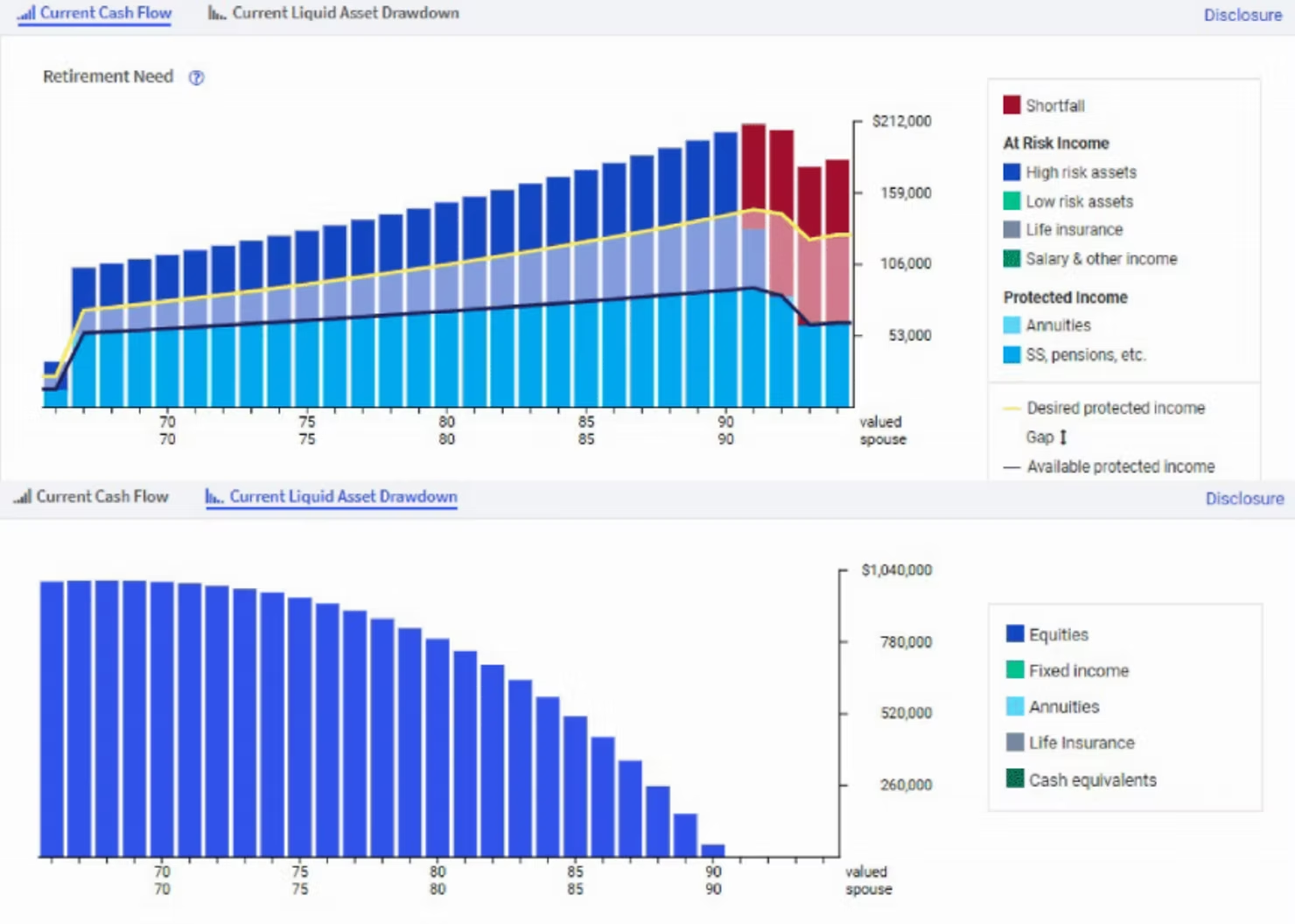

Let’s examine this couple’s retirement plan under a 2% inflation rate assumption.

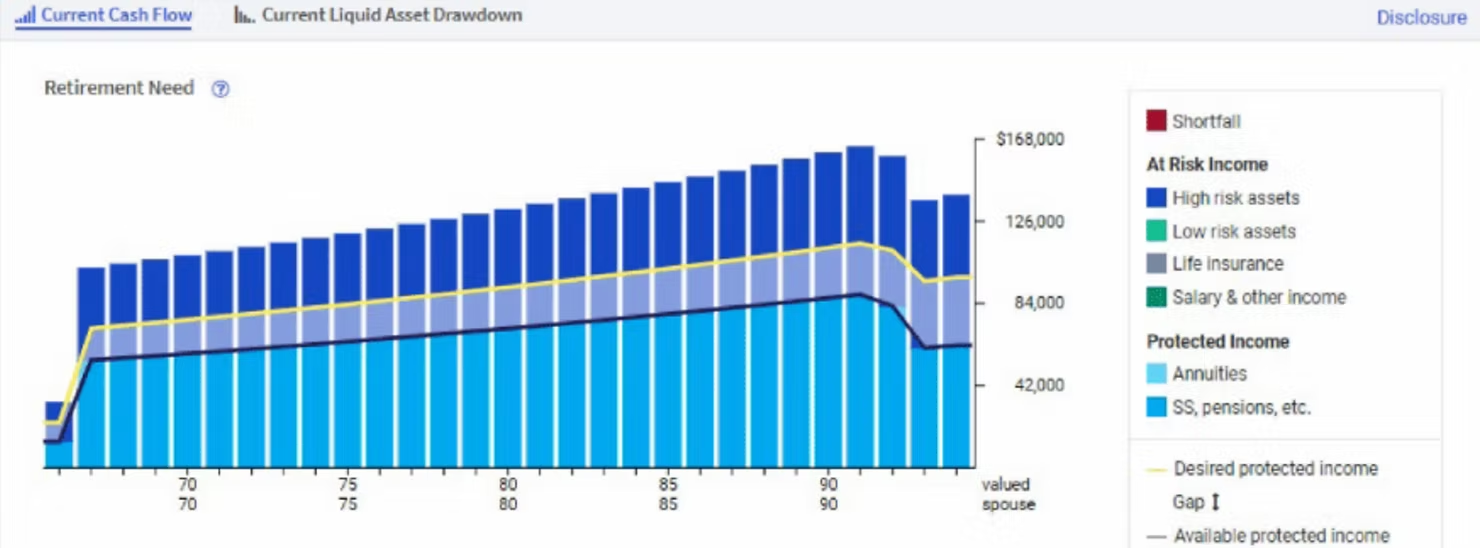

The Impact of a 2% Inflation Rate: Their Income Statement

First, let's create a projection that assumes a 2% annual inflation rate applied to their $100,000 income goal, below the historical average of 2.9%. The chart below provides a detailed view of how this couple’s income and assets are managed with their current financial plan over time.

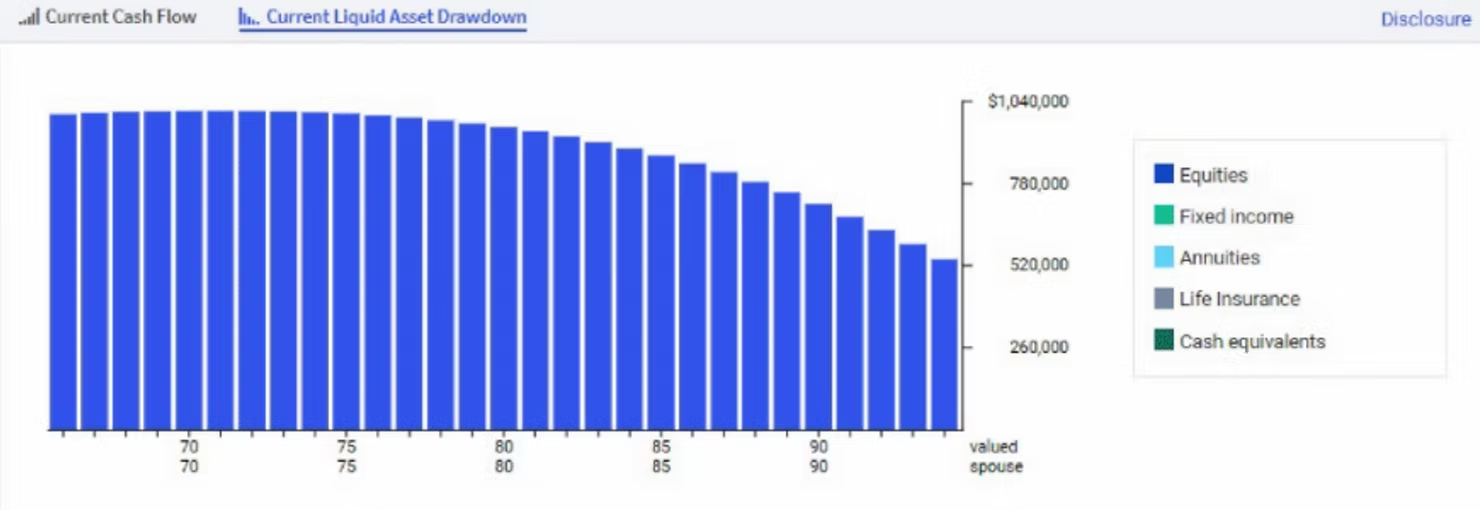

Portfolio Performance at 2% Estimated Inflation: Their Balance Sheet

This chart shows what the couple’s current asset base would be throughout their retirement years:

Despite withdrawals, the portfolio retains a balance of $500,000 by the time the wife is projected to pass away at age 95. This provides a cushion for unexpected expenses throughout their retirement or an inheritance for their children.

But what if we made one minor adjustment to the inflation rate?

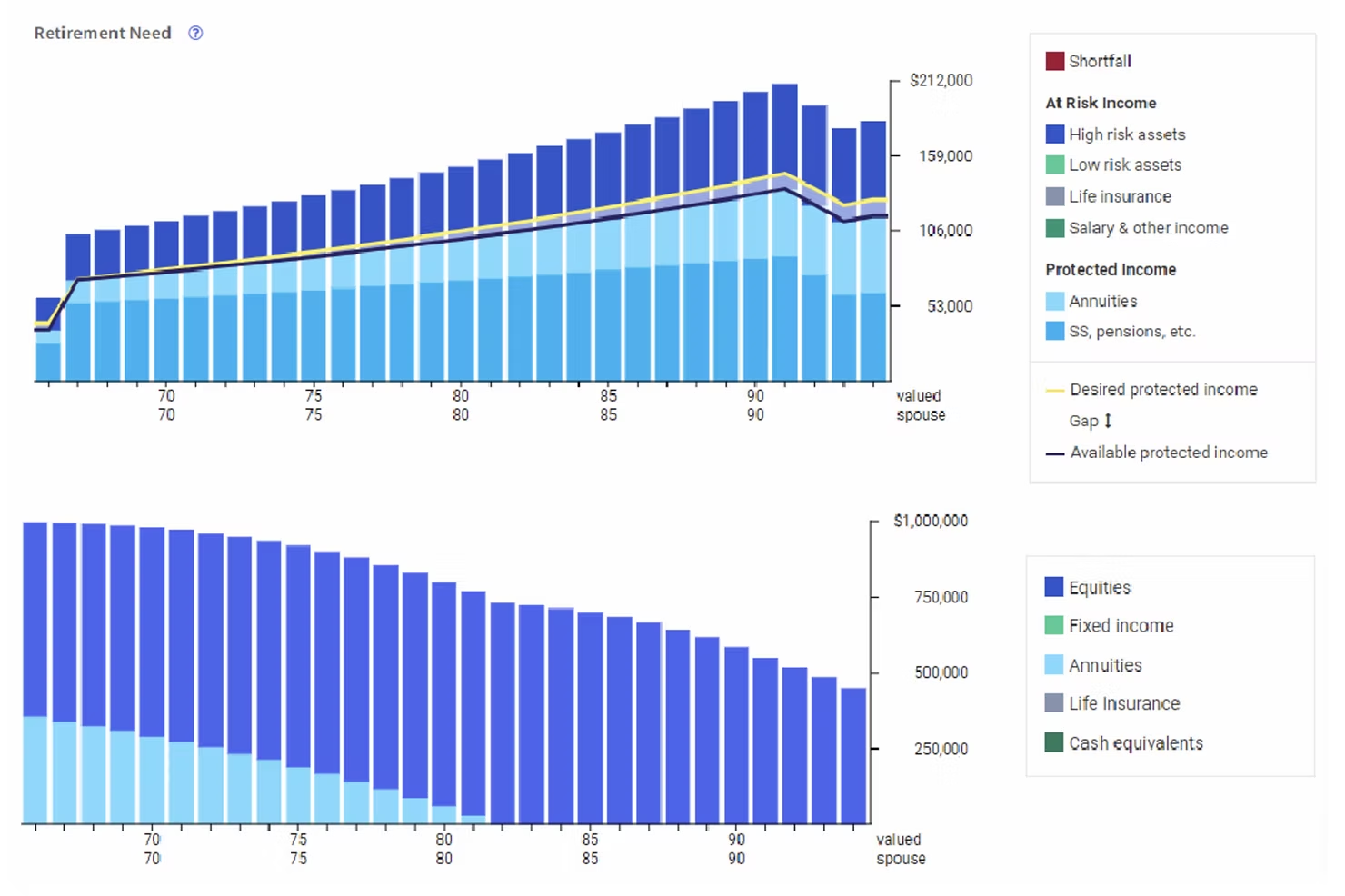

The Impact of a 3% Inflation Rate

What if we account for inflation at 3% instead of 2%, aligning more closely with the historical average inflation rate of 2.9%? It doesn't seem like much of a change, but here’s how this minor shift impacts the couple’s financial plan:

In reality, most clients won't just run out of money and have a shortfall. A prudent advisor would help them adjust their spending in response to rising inflation along the way, but these conversations can be challenging. For example, advising clients to cut their annual expenses by $10,000–$25,000 due to underestimated inflation is far from ideal.

Inflation’s impact may be even more pronounced in specific expense categories, such as healthcare or real estate, which can see annual increases of 4% or 5% or even exceed recent averages of 5% to 8% per year, leading to permanently elevated costs.

How Advisors Can Protect Clients Against Future Impacts of Higher Inflation

How can you position your client to protect against a higher inflation rate than what you’ve been using in your plans for the last decade or two? Here are two things you can recommend your clients do to protect against the future impact of higher inflation:

Let’s dive deeper into how we could apply these concepts to this client’s financial plan.

Purchase an Increasing Income Annuity

To protect against the impacts of inflation, this client can buy an increasing income annuity, removing $385,000 from the $400,000 sitting in fixed income.

We’ll allocate the $385,000 to a joint lifetime income annuity with an increasing income feature. This will generate $16,000 in joint lifetime income with annual increases, bridging the gap between the client’s protected income target and current income sources. This increases their previously protected income amount of $54,000 to their goal of $70,000.

While a level income annuity might require a smaller upfront investment (potentially $350,000), an increasing income feature will also provide vital protection against the compounding effects of inflation over time.

Reallocate Remaining Assets Toward Equities

With the annuity covering the client’s protected income needs, the remaining fixed-income assets ($15,000) can be reallocated to equities. This shift allows the portfolio to capitalize on the long-term higher growth potential of equities, which can also act as a hedge against inflation.

By doing this, we effectively reduce the reliance on a traditional 60/40 portfolio. Since the annuity now serves as a fixed-income alternative (providing stability and systematic monthly income), the remaining equity allocation can focus on non-protected expenses and long-term growth.

Within the planning software, this adjusted plan replaces the previous approach:

How do these adjustments translate into the client example’s financial plan under the 3% inflation rate scenario?

Implementing These Adjustments in Client Retirement Plans

By incorporating an increasing income annuity and reallocating the remaining assets to equities, here’s how the client's financial plan evolves:

Meeting Protected Income Goals

With inflation at 3%, the first priority is ensuring 70% of the couple’s income needs are covered by guaranteed sources like Social Security and annuities. By incorporating an increasing income annuity, their protected income aligns with their $70,000 goal. This adjustment reduces pressure on the equity side of the portfolio, leaving $615,000 in assets and only $30,000 needed annually to meet remaining income "wants" versus "needs."

Avoiding Portfolio Depletion

Under the previous plan, higher inflation depleted their portfolio five years before the wife reaches age 95. However, with the increasing annuity in place and a strategic shift of remaining assets to equities, the revised plan not only meets all expendable income demands but also preserves $250,000 by the end of retirement. The red bars are gone!

Achieving Additional Client Goals

This change swung a -$1,000,000 shortfall back to a $250,000 gain, still at the 3% inflation "stress." Reverting back to the 2% baseline inflation assumption, the client would now have an excess of $1,6000,000. Now, you can see how these adjustments open new possibilities. With a safer cash flow plan, clients can:

When the client is transferring money from their current fixed-income options into a more efficient increasing fixed-income option, it’s going to benefit their portfolio in bad, average, and good scenarios. In down markets, the annuity ensures stable income, reducing reliance on underperforming equity assets. In up markets, a higher equity allocation captures more growth. In average markets, the portfolio outperforms the original plan due to the efficient reallocation of fixed-income assets to an increasing income annuity.

Conclusion

By reallocating $385,000 from fixed income to an increasing income annuity and reallocating their remaining assets towards equities, the couple achieves their goals:

Even under higher inflation, a proactive approach can transform retirement planning from a concern into an opportunity, providing clients peace of mind and financial freedom.

--

Core Income is an FMO, IMO, and independent insurance brokerage dedicated to serving financial advisors, their staff, and their clients.

Our mission is to help advisors deliver financial certainty by supporting them through actuarial precision, elite responsiveness, and collaborative partnerships.

To learn more about how we can support you, schedule a consultation with our team or call us at 800.541.7713.

Stay connected with us on social media for more tips and insights on annuities, life insurance, and long-term care.

According to a comprehensive study by the Transamerica Center for Retirement Studies, a leading research organization in retirement planning, only...

Our suite of risk management tools designed to help advisors enhance their retirement planning strategies and navigate client portfolios with...

For certain clients, particularly those with little risk of outliving their assets, claiming benefits earlier can result in higher lifetime wealth,...